Demystifying IR35: A conversation with our IR35 expert, Alex Moore

In the labyrinth of tax regulations and employment laws, one particular term stands out for its notoriety and complexity: IR35.

In true Buzz form, we wanted to provide clarity on the resourcing intricacies that businesses often face and highlight how these can be successfully addressed. The Buzz is legally and operationally structured to protect clients from potential implications around IR35, so we invited our Contracting Consultant & IR35 expert, Alex Moore, to decode the legislation and to share how businesses like The Buzz are designed to bring together companies and experienced flexible resource, when it’s needed and with no risk.

So, what is IR35?

IR35, also known as the ‘Intermediaries Legislation’, and more recently ‘off-payroll working’, is tax legislation which came into effect in April 2000. It’s designed to combat tax avoidance by individuals who supply their personal services to clients via their own Limited Company business, commonly referred to as a Personal Service Company (PSC).

In essence, if a contractor is completing work for a client and they look and feel like an employee of the client, they are ‘caught’ by the legislation. This is commonly referred to as ‘inside IR35’ with HMRC deeming them as a ‘disguised employee’. This means that any income received for that assignment should have full Income Tax and National Insurance Contributions (NICs) deducted at source by the fee payer, as if they were an employee.

There are many factors to consider when assessing a contractors IR35 status including:

- Control the client has over the contractor and their work – In most cases where professional services are provided, it’s important a contractor can demonstrate a certain amount of autonomy in the way they undertake a project. Employees are typically directly supervised and controlled by their employers. The truly self-employed, however, will be able to influence how they complete work they have been hired to do. For a contractor to successfully demonstrate that they are not under direct supervision and control, both the written contract and working practices must show that the client cannot influence how they carry out their services, nor the manner in which they are performed.

- Right of substitution – The right to provide a substitute has long been deemed key when demonstrating that a contract assignment falls outside IR35 scope. An employee provides his/her personal services to an employer (client), whereas a business would provide its services to a client, not the exclusive services of an individual. So, in effect, a contractor could substitute themselves when unwell or on holiday, sending another individual from their business to perform the contract.

- Mutuality of obligation – This exists when an employer expects a worker to undertake work when asked to do so, and the worker expects to be given work on a constant basis. For self-employed people, they would expect a client to hire them to undertake a specific task/scope, with no expectation of further work being provided after the initial task/scope expires.

- Financial risk – The contractor and their Limited Company can be liable for certain financial exposure. For example, if a roofer fitted a new roof which leaked a month later, they’d be liable to fix the roof at their own cost and on their own time.

- Being part and parcel of the client’s organisation – A contractor shouldn’t have access to employee benefits, such as a sick pay, pensions, employee rights, etc.

Prior to the legislation changes, the responsibility of determining a contractors IR35 status fell on the contactor and any tax liabilities for failing to operate IR35 correctly also lay with the contractor and their Limited Company.

What’s changed?

Since the Off-Payroll changes that were made in 2017 and 2021, the landscape is a bit different. The factors for determining someone’s IR35 status are the same, however, the party in the supply chain responsible for making that determination and where the liability sits has shifted.

In the public sector, the determination for IR35 moved to the End Client (the company at which the contractor carried out the work) and the liability falls on the fee payer (the company in the supply chain that actually pays the Limited Company).

The same changes came into effect in the private sector in 2021. If the End Client determines a role as ‘outside of IR35’ then a contractor can continue the contract as before, with gross payments being paid into the Limited Company. However, if a client determines an assignment as ‘inside IR35’, HMRC will no longer allow gross payments into a Limited Company and PAYE Tax and National Insurance must be deducted at source.

All contractors and clients in the Public Sector fall under the above changes, however, in the Private Sector this change only impacts medium and large business and not those deemed as ‘small’ under the Companies Act 2006. This relates to the End Client and not the Fee Payer or the Limited Company. A ‘small’ business is one that satisfies two or more of the following:

- An annual turnover not exceeding £10.2m

- A balance sheet total not more than £5.1m

- An average of no more than 50 employees in that financial year

How has this impacted the industry and are there solutions?

As with any legislation change in the contracting sector, there was an initial risk adverse reaction from businesses who feared an IR35 investigation from HMRC and the potential tax bill that could come with it. Post April 2021, the market saw many private sector companies either disengaging Limited Company contractors altogether, or blanket determining everyone as inside IR35 to eliminate the risk. This led to several problems for businesses including, a lack of flexible resource, a lack of expertise from experienced contractors and/or an increase in costs, as they were forced to engage contractors on inside IR35 assignments, with higher pay rates.

However, this risk adverse ‘blanket’ approach isn’t the only option as there are compliant scenarios still available for businesses to engage experienced Limited Company contractors on flexible terms and without risk.

In 2020, The Buzz was conceived around the idea of bringing together a collective of readily available, experienced real estate marketers who could offer solutions for organisations in and around the sector. By pro-actively seeking specialist advice, The Buzz ensures that they take a pragmatic IR35 approach with detailed understanding of the legislation and engagement of marketeers via compliant supply chains that completely eliminate client risk.

IR35’s current impact on supply chains

To determine the ultimate End Client we need to understand where responsibilities lie. The End Client is the party in the supply chain where the contractor carries out the services and there are many different scenarios but let’s look at two of the most common.

Scenario 1: Recruitment Agencies

Firstly, the most familiar supply chain where IR35 is considered is Client through to Recruitment Agency through to Limited Company contractor. The Recruitment Agency purely supplies ‘people’, and in this case ‘contractors’ to the End Client and is not providing a service. So the Limited Company is actually providing a service to the End Client under their own Limited Company. The End Client is then liable to make the determination for IR35 and the Recruitment Agency, as the fee payer, is liable to enact the IR35 determination. If the contractor is not providing a personal service to the client, but is providing a business-to-business service (determined as above), then they can be deemed outside IR35 and operate through their Limited Company without any change.

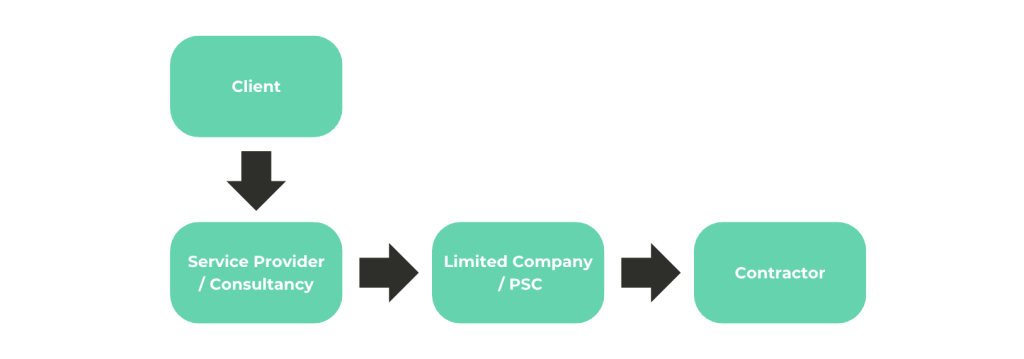

Scenario 2: Outsourced Providers

The next scenario is slightly more complex but demonstrates the reality of the supply chain that outsourced providers (OP) fall within.

The big difference in this supply chain is that the recruitment agency has been replaced by an outsourced provider (such as The Buzz). Unlike the recruitment agency, the OP is providing a genuine business-to-business service to the client via scopes of work, work packages, retainers etc and not just individuals as the recruitment agency would.

How The Buzz is perfectly positioned to support your flexible marketing needs

With clients looking for more flexible ways of resourcing their marketing, The Buzz’ unique approach ensures seamless support tailored to clients’ specific requirements.

By leveraging The Buzz, clients benefit from a streamlined process that can mobilise quickly without the hassle and fees of traditional recruitment. As a marketing agency offering a wide range of marketing services, The Buzz becomes the End Client in the supply chain. When The Buzz engages their collective of marketing contractors to carry out services for a client, that client has no responsibility for IR35 determinations. This removes hassle and importantly, potential tax liabilities. It also allows clients to confidently continue to use flexible sector expertise resource that they may not have in-house and that The Buzz will ensure that all agreed scopes of work or retainers are carried out.

While the private sector IR35 changes loom large, The Buzz’ ‘Small’ Company classification means they are exempt from the 2021 Off Payroll changes with original IR35 legislation applying, meaning contractors are responsible for determining their own IR35 status and liabilities.

Additionally, on 6th April 2024, there was a further update to IR35, the IR35 offset. Whilst this reduces (but does not eliminate) potential tax bills for some end clients impacted by IR35, it has no impact on The Buzz’ clients who remain totally risk free.

To safeguard both The Buzz and our contractors, we’ve partnered with Sapphire on a consultancy basis to ensure IR35 compliance, minimising risks for all parties involved. Clients can therefore rely on The Buzz as a trusted partner for flexible, compliant marketing solutions.

Alex Moore is a Business Development Director with over 15 years’ experience in the contracting sector and works for Sapphire, specialists in the Contracting, Accounting and Payroll sector. Alex has been working alongside The Buzz since 2022 to provide ongoing legislation and tax advice to ensure the business functions as a fully flexible and compliant marketing solution.

If you would like more information on IR35 and how it affects you or your business, get in touch with us at hello@thebuzz.marketing